Market volatility is exhausting. One week the stock market is hitting all-time highs, and the next, a single inflation report sends index funds tumbling. For money you absolutely cannot afford to lose—like a down payment on a house, an emergency fund, or your baseline retirement income—playing the equity lottery isn’t an option.

You need safety, but leaving cash in a standard savings account means losing purchasing power to inflation.

The solution isn’t a secret Wall Street algorithm. It is a time-tested, straightforward strategy called laddering. By staggering the maturity dates of Certificates of Deposit (CDs) and government bonds, you can lock in high yields, maintain steady liquidity, and completely eliminate market risk.

Here is exactly how to build one.

The Core Concept: What is a Laddering Strategy?

When you buy a long-term fixed-income asset, you face two main risks:

- Liquidity Risk: Your money is locked up. If you need it early, you pay a penalty.

- Interest Rate Risk: If you lock in a 4% yield for five years, and rates jump to 6% next year, you are stuck missing out on better returns.

Laddering solves both problems. Instead of putting all your money into a single 5-year CD or bond, you divide your capital into equal slices and buy assets that mature at staggered intervals (e.g., 1 year, 2 years, 3 years, etc.).

Every year, a portion of your money matures, giving you a pool of liquid cash. If you don’t need the money, you reinvest it at the longest end of the ladder. If interest rates have gone up, you get to capture those higher yields without waiting years for your entire portfolio to unlock.

CDs vs. Treasury Bonds: The Building Blocks

You can build a ladder using exclusively bank CDs, exclusively government bonds, or a hybrid of both. Here is how to choose:

- Certificates of Deposit (CDs): Issued by banks and insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor, per institution. They offer absolute principal protection but are often subject to early withdrawal penalties. You can compare current competitive rates via platforms like Bankrate.

- U.S. Treasury Bonds: Backed by the full faith and credit of the U.S. government. They are entirely safe from default and, crucially, exempt from state and local income taxes. This makes Treasuries highly efficient if you live in a high-tax state like California or New York. You can purchase them directly through TreasuryDirect.

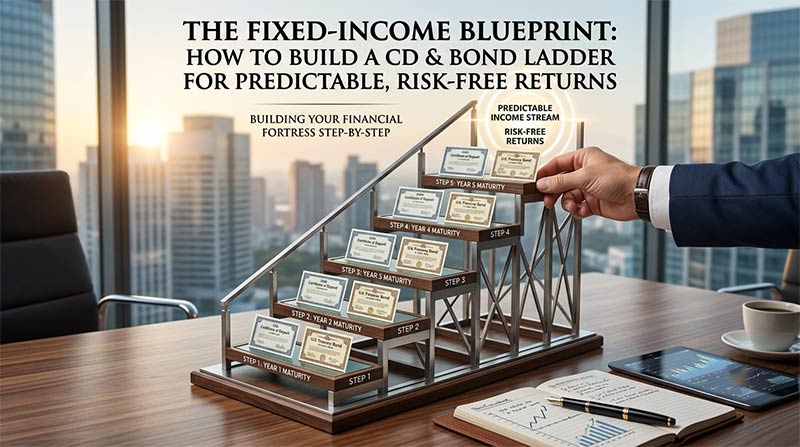

Anatomy of a 5-Year Hybrid Ladder

Let’s look at a practical example. Suppose you have $50,000 in cash that you want to protect and grow over the next five years. Instead of dumping all $50,000 into a single account, you split it into five equal tranches of $10,000.

Here is how that allocation looks at day one:

Year 1: Initial Set-Up

| Asset Type | Allocation | Maturity Term | Purpose / Execution |

| High-Yield CD | $10,000 | 1 Year | Quick liquidity; captures short-term high rates. |

| U.S. Treasury Note | $10,000 | 2 Years | Balanced yield; state-tax exempt protection. |

| U.S. Treasury Note | $10,000 | 3 Years | Mid-term stability; locks in current yields. |

| High-Yield CD | $10,000 | 4 Years | Higher yield potential for a slightly longer commitment. |

| U.S. Treasury Note | $10,000 | 5 Years | Maximizes yield lock-in; protects against dropping rates. |

The “Rollover” Mechanical Motion

What happens when Year 1 ends?

Your first $10,000 CD matures. You take that cash and reinvest it into a new 5-year asset.

Simultaneously, your original 2-year Treasury note now has only 1 year left until maturity. Your 3-year note has 2 years left, and so on. Without doing any extra work, your portfolio has maintained its structure: you now have an asset maturing every single year, but you are constantly buying into the highest-yielding 5-year bracket.

The Advantages of the Ladder Structure

1. Guaranteed Peace of Mind

Unlike stocks or real estate, your principal does not fluctuate based on market sentiment. You know to the penny what your portfolio will be worth on any given maturity date.

2. Predictable Cash Flow

If you are living off your savings or supplementing retirement income, a ladder acts like a predictable paycheck. You can align your maturity dates with major expected expenses (e.g., college tuition, property taxes).

3. Protection Against Rate Environments

- If rates rise: You have cash maturing soon to reinvest at those higher rates.

- If rates fall: You have already locked in higher yields for the next 3 to 5 years on the longer rungs of your ladder.

Pitfalls to Avoid

While laddering is incredibly safe, it isn’t entirely foolproof. Keep these nuances in mind:

- The Inflation Trap: Fixed income protects your nominal cash, but if inflation spikes higher than your average yield, your real purchasing power declines. Never put 100% of your long-term wealth into fixed income; use ladders for your defensive capital.

- Brokered CDs vs. Bank CDs: If you buy a CD through a brokerage account (like Vanguard or Charles Schwab), you can sell it early on the secondary market without a bank penalty. However, if interest rates have risen, you might have to sell that brokered CD at a slight loss. Stick to traditional bank CDs if you want absolute certainty of getting your exact principal back before maturity.

- Call Risk: Some CDs and bonds are “callable,” meaning the issuer can force-redeem them early if interest rates drop. Read the fine print: always prioritize non-callable assets for your ladder to ensure your yield is locked for the full duration.

Want to Make Money From Home ?

Join 55,000+ real, remote ways to make money every week.

Good luck! I hope you find the perfect remote opportunity for your lifestyle and goals.