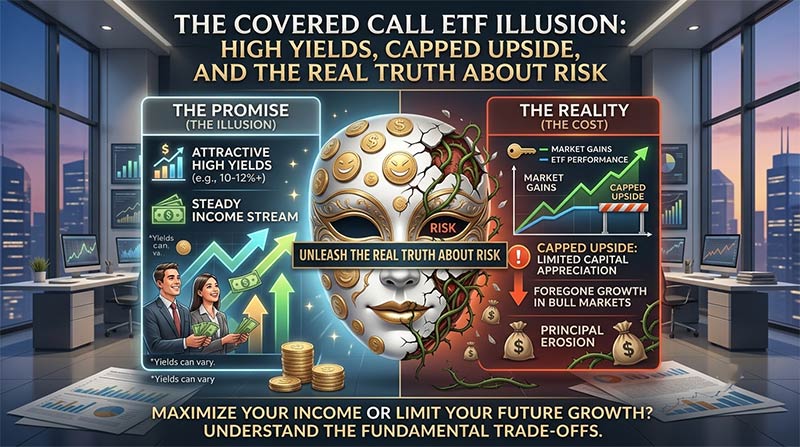

Walk into any online investing forum today, and you will see the same tickers thrown around like confetti: JEPI, JEPQ, SPYI. The promise is intoxicating. Why settle for a meager 1.3% dividend yield from a traditional S&P 500 index fund when you can collect an 8% to 12% annualized cash flow from a covered call ETF?

Even better, marketing materials often frame these vehicles as a way to manufacture “higher income without extra risk.”

But let’s be perfectly candid: Wall Street doesn’t hand out free lunches. While covered call ETFs are phenomenal tools for specific financial goals, they do not eliminate risk—they simply reshape it. To use them effectively, you have to understand exactly what you are trading away to get those massive monthly distributions.

The Mechanics: How Covered Call ETFs Generate Cash

To evaluate the true risk of these funds, you first need to see how the sausage is made. A standard covered call ETF uses a simple two-step strategy executed at scale:

- The Long Position: The fund buys a basket of stocks (such as the constituents of the S&P 500 or the Nasdaq-100).

- The Option Overlay: The fund writes (sells) call options against those exact stocks.

When the fund sells these options to speculators, it collects an immediate cash payment called a premium. This premium is what gets passed along to you as a juicy monthly dividend. For an in-depth breakdown of how individual options function, you can read Investopedia’s comprehensive guide to covered calls.

Deconstructing the Myth: Is It Really “Without Extra Risk”?

When analysts say these funds have “no extra risk,” they usually mean the fund isn’t using leverage, borrowing money, or shorting stocks—tactics that can wipe out a portfolio overnight. In that strict sense, they are correct. Your immediate downside risk is actually a tiny bit lower than a standard index fund because the option premium you collect acts as a small cushion.

However, looking only at nominal downside risk ignores the two actual traps of the strategy: uncapped downside and strictly capped upside.

1. The Asymmetric Downside

If the underlying stock market plummets 20% in a sudden correction, a covered call ETF will also plummet. If the fund collected a 1.5% premium that month, its net loss is still 18.5%. The strategy protects you from a minor market paper cut, but it provides virtually no protection against a broken leg.

2. The Opportunity Cost Risk (Capped Growth)

This is where the hidden risk hurts long-term investors. By selling a call option, the ETF promises to sell its underlying stocks if they rise above a specific price (the strike price). If the tech sector rips upward by 10% in a single month, the ETF misses out on the vast majority of that growth because its upside was legally surrendered to the option buyer.

Over a multi-year bull market, this cap creates severe underperformance relative to a simple buy-and-hold strategy.

Comparing the Strategies: Index vs. Covered Call Funds

To see how this trade-off plays out across different fund styles, look at the structural differences below:

| Strategy Type | Core Goal | Distribution Yield (Avg.) | Performance in a Ripping Bull Market | Performance in a Severe Market Crash |

| Standard Index Fund (e.g., SPY) | Total Return & Capital Growth | ~1.3% | Captures 100% of market gains. | Takes 100% of market losses. |

| Full-Overwrite ETF (e.g., QYLD) | Maximum Immediate Income | 10% – 12% | Poor. Misses almost all capital appreciation. | Takes full losses, mitigated slightly by premium income. |

| Active/Partial Overwrite (e.g., JEPI) | Balanced Income & Defensive Growth | 7% – 9% | Moderate. Captures a portion of market upside. | Outperforms the index slightly due to lower beta and high premium cushions. |

When Do Covered Call ETFs Actually Make Sense?

Because of this specific trade-off, covered call ETFs are not a “set-it-and-forget-it” replacement for your core equity holdings if you are a younger investor trying to grow a retirement nest egg. Instead, they thrive in highly specific scenarios:

- Sideways or Flat Markets: If the stock market goes nowhere for two years, a standard index fund returns 0%. A covered call fund, however, keeps grinding out steady monthly yields from option premiums, drastically outperforming the broader market.

- The Retirement Distribution Phase: If you are actively living off your portfolio, these funds are incredibly useful. They generate organic cash flow, preventing you from being forced to sell your underlying stock shares at a loss during a down market to pay your bills.

- Volatile but Range-Bound Environments: High market volatility inflates option premiums. When markets are choppy but not entering a secular bear market, these funds collect their highest yields.

How to Integrate Them Wisely

If you want to add these vehicles to your investment mix, treat them as an income sleeve rather than a wealth-compounding engine.

Many seasoned investors allocate a minority portion (e.g., 10% to 20%) of their capital to hybrid income generators like the JPMorgan Equity Premium Income ETF (JEPI) to provide stable, reliable cash flow. The remaining bulk of their portfolio stays in low-cost, uncapped index funds to capture long-term compounding.

Before buying, look closely at the fund’s prospectus. Funds that write out-of-the-money options or only overwrite a portion of their portfolio tend to preserve your principal capital much better over a market cycle than funds that sell full, at-the-money call options.

Want to Make Money From Home ?

Join 55,000+ real, remote ways to make money every week.

Good luck! I hope you find the perfect remote opportunity for your lifestyle and goals.

Disclaimer and Risk Warning

Financial Disclaimer: The content published on this page is intended solely for educational, informational, and editorial purposes and does not constitute formal financial, legal, tax, or investment advice. The financial thresholds, metrics, and strategies outlined are generalized guidelines and may not align with your specific financial goals, time horizons, or personal risk tolerances.

Risk Warning: All forms of financial investment—including traditional public stocks, foreign exchange trading, digital real estate crowdfunding, and alternative trust investments—carry inherent risks, including the potential loss of your entire initial principal. Payout yields, dividend distributions, and platform interest rates are never legally guaranteed and can be reduced, frozen, or entirely dissolved at any time without warning. Past performance does not serve as a reliable indicator of future market movements. Always perform meticulous independent due diligence or consult with a certified, fiduciary financial advisor before deploying capital into any market.