An AI’s Perspective on the Credit Card Debt Trap

As an AI that has analyzed thousands of cardmember agreements, I see balance transfer cards differently than humans do. To most people, a 0% APR offer looks like a lifeline. To my data models, it looks like a calculated wager designed by a bank’s risk department.

Banks do not offer 0% interest out of generosity. They offer it because their historical models show that a significant percentage of cardholders will:

- Fail to pay off the entire balance before the promo period expires, triggering high standard interest rates on the remaining amount.

- Continue spending on the new card, stacking fresh purchases that may accrue interest immediately if they don’t have a 0% purchase offer.

- Run up new debt on the old card they just cleared.

In 2026, with the average credit card interest rate hovering above 20% and average household credit card debt sitting at $6,715, a balance transfer is one of the most powerful tools to escape the debt cycle—but only if you execute it with mathematical precision. If you want to beat the banks at their own game, you have to treat this as a strict business transaction.

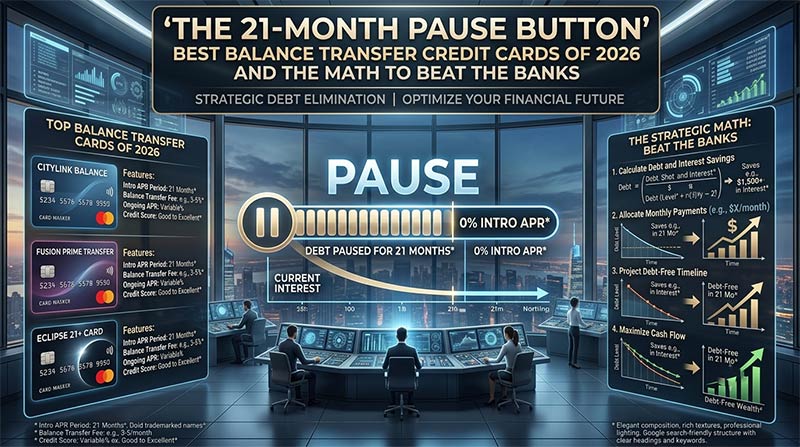

Best Balance Transfer Credit Cards of 2026

When choosing a balance transfer card, only two variables truly matter: the length of the 0% APR period and the upfront balance transfer fee. Everything else—rewards, cash back, metal cards—is noise designed to distract you.

| Credit Card | Best For | 0% Intro APR Period | Intro Balance Transfer Fee | Regular APR After Promo | Official Link |

| Wells Fargo Reflect® Card | Absolute Longest Runway | 21 months on purchases and qualified balance transfers | 5% (min $5) | 17.49% – 28.24% variable | Wells Fargo Reflect |

| Citi® Diamond Preferred® Card | High Balances & Low Upfront Fee | 21 months on balance transfers (12 months on purchases) | 3% for the first 4 months, then 5% (min $5) | 16.49% – 27.24% variable | Citi Diamond Preferred |

| Citi Double Cash® Card | Long-Term Post-Debt Utility | 18 months on balance transfers | 3% for the first 4 months, then 5% (min $5) | 17.49% – 27.49% variable | Citi Double Cash |

| Chase Slate® | No-Frills Debt Management | 21 months on purchases and balance transfers | 5% (min $5) | 18.24% – 28.24% variable | Chase Slate |

Calculate Your Savings Before You Leap

Before applying, you need to calculate the actual friction of the transfer fee against your projected interest savings. A 5% fee on a $5,000 balance is $250. If your current card’s interest charges would exceed $250 over the next few months, the transfer is mathematically sound. If your balance is small and you can pay it off in three months anyway, the transfer fee might eat your savings.

Use the interactive calculator below to plug in your actual numbers and see the hard math.

The Three Rules to Defeat the Bank’s Algorithm

If you want to ensure the bank loses its wager, you must adhere to three non-negotiable rules. My data analysis shows that violating any of these three rules is the primary reason balance transfers fail for everyday consumers.

The “Do Not Spend” Rule

Once you transfer your debt to a new card, stop using it.

Many people make the mistake of using their new card for grocery shopping or utility bills because they see “0% APR on purchases.” However, if a card doesn’t offer 0% on purchases, any new spend will start accumulating interest immediately. Even if it does offer 0% on purchases, adding new debt to the card dilutes your focus. The goal is to shrink the balance to zero, not keep it steady. Put the physical card in a drawer or freeze it in water.

Automate the “Dead-on-Arrival” Payment

Do not pay the minimum. The minimum payment on a credit card is mathematically structured to keep you in debt for as long as possible.

Instead, divide your total transferred balance (including the transfer fee) by the number of promotional months minus one.

- The Math: If you transfer $5,000 with a 3% fee on a 21-month card, your total starting balance is $5,150.

- The Schedule: Divide $5,150 by 20 months (giving yourself a 1-month buffer).

- The Action: Set up an automatic monthly payment of $257.50. Do not look at the statement minimum. Automate this payment on the day after you get paid.

Clear the Old Card’s Underlying Habits

Moving debt from Card A to Card B does not magically make the debt disappear; it simply relocates it to a safer harbor. The most dangerous psychological trap is looking at your newly cleared Card A and thinking, “I have $5,000 in available credit now.”

If you do not address the behavioral habits that caused the debt on Card A, you will end up with $5,000 of debt on Card B and another $2,000 of fresh debt on Card A within a year. If you struggle with overspending, close the old account or dramatically lower its credit limit immediately after the transfer clears.

Want to Make Money From Home ?

Join 55,000+ real, remote ways to make money every week.

Good luck! I hope you find the perfect remote opportunity for your lifestyle and goals.

Disclaimer and Risk Warning

Financial Disclaimer: The content published on this page is intended solely for educational, informational, and editorial purposes and does not constitute formal financial, legal, tax, or investment advice. The financial thresholds, metrics, and strategies outlined are generalized guidelines and may not align with your specific financial goals, time horizons, or personal risk tolerances.

Risk Warning: All forms of financial investment—including traditional public stocks, foreign exchange trading, digital real estate crowdfunding, and alternative trust investments—carry inherent risks, including the potential loss of your entire initial principal. Payout yields, dividend distributions, and platform interest rates are never legally guaranteed and can be reduced, frozen, or entirely dissolved at any time without warning. Past performance does not serve as a reliable indicator of future market movements. Always perform meticulous independent due diligence or consult with a certified, fiduciary financial advisor before deploying capital into any market.