Most personal finance advice is a trap. It asks you to track every single cup of coffee, log receipts into a spreadsheet, and feel a pang of guilt every time you spend money.

Here is the truth: traditional budgeting fails because it relies on willpower. Willpower is a finite resource. If you have to make an active decision to save money, invest, or pay bills every single month, you will eventually slip up.

The “lazy but smart” approach turns this on its head. Instead of relying on discipline, you rely on a system. By engineering an automated cash flow pipeline, you ensure your money goes exactly where it needs to go—without you ever having to lift a finger or look at a spreadsheet.

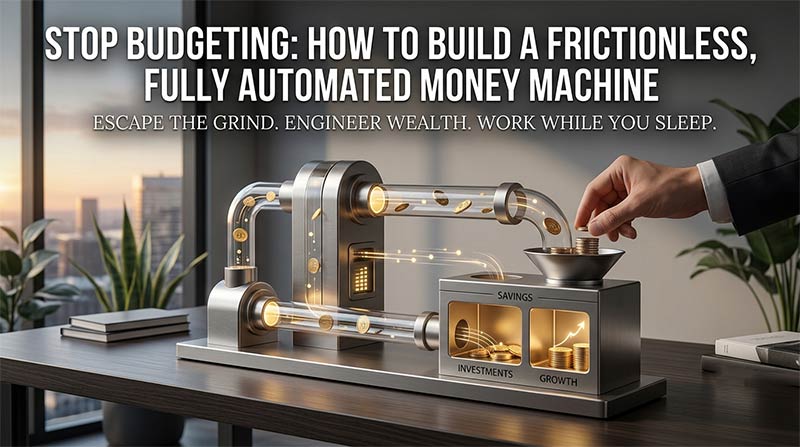

The Anatomy of an Automated Money Pipeline

An automated financial system works like a water treatment plant. Money flows into a central reservoir (your primary checking account) and is immediately diverted through specialized pipes into different tanks: bills, short-term savings, and long-term investments.

The goal is to map out these percentages before the money hits your account.

As shown in the framework above, your primary checking account acts as the central traffic controller, distributing funds dynamically so your fixed costs, savings goals, and guilt-free spending money never mix.

The Step-by-Step Setup

Building this machine takes about an hour of upfront effort. Once it is running, your only job is to let it work.

1.Establish Your Central Hub:Step 1。

Choose a checking account with zero fees and robust external transfer capabilities. This is where your direct deposit from your job must land. If you work a regular 9-to-5, set up your payroll to split your check automatically if they offer it, otherwise land 100% of it here.

2.Route Your Fixed Bills:Step 2。

Log into every recurring bill provider (rent, utilities, insurance, phone) and switch them to auto-pay. For maximum credit card rewards, map these bills to a primary cashback card, and set that credit card to auto-pay its full statement balance from your central checking account every month.

3.Skim Off Your Savings First:Step 3。

Set up a recurring transfer to happen one day after payday. This transfer moves money from your checking account into a High-Yield Savings Account (HYSA) like Ally Bank or Marcus. If you never see the money in your checking account, you won’t count it as available spending cash.

4.Automate Your Future Wealth:Step 4。

Link your checking account to an investment platform like Vanguard or Fidelity. Set an automatic monthly buy order for broad-market index funds or ETFs. This eliminates the temptation to “time the market” and ensures you consistently benefit from dollar-cost averaging.

The Lazy Investor’s Tool Matrix

You do not need dozens of apps to manage this system. In fact, fewer moving parts mean fewer points of failure. The ideal stack consists of a smart aggregation tool to track the big picture and financial institutions that support automated rules.

The table below breaks down the best-in-class tools for keeping your money on autopilot based on what you actually need them to do.

| Tool Category | Top Platforms | What It Automates | Why It’s “Lazy But Smart” |

| The Blueprint Hub | Monarch Money, Copilot | Cross-account tracking and net worth monitoring. | Syncs everything in one dashboard so you can spot broken links in your pipeline instantly. |

| Automated Saving | Wealthfront, Ally Bank | Bucket creation and automatic rate optimization. | Let’s you create “sub-accounts” (e.g., Travel, Taxes) that auto-fill via rules. |

| Hands-Off Investing | Betterment, Acorns | Portfolio rebalancing and dividend reinvestment. | Automatically invests your spare change or monthly allocations into optimized portfolios. |

The “Guilt-Free” Secret

The best side effect of an automated cash flow system is the complete elimination of financial guilt.

When your system is built correctly, whatever money remains in your checking account at the end of the automation cycle is yours to spend entirely as you please. Because your bills are already paid, your retirement is funded, and your savings goals are growing on autopilot, you can spend that remaining cash on dinners, travel, or hobbies with absolute peace of mind.

You aren’t ignoring your finances; you are simply managing them like a machine. For deep-dive blueprints on this specific philosophy, resources like Ramit Sethi’s Personal Finance Systems offer incredible frameworks for designing a rich life without the cognitive load of traditional budgeting.

Want to Make Money From Home ?

Join 55,000+ real, remote ways to make money every week.

Good luck! I hope you find the perfect remote opportunity for your lifestyle and goals.