The investing landscape of 2026 requires a hard pivot in how we think about cash flow. With the broader U.S. stock market up more than 20% over the past twelve months, finding true value has become an exercise in avoiding crowded trades. While tech mega-caps have spent the last two years normalizing their newly minted dividend policies, a quiet divergence has opened up: traditional, wide-moat dividend growers have been left lagging behind the valuation expansion, creating a generational buying opportunity for long-term wealth builders.

Chasing the highest absolute yield right now is an unforced error. True financial freedom isn’t built on a static 8% yield that gets cut at the first sign of a macroeconomic slowdown; it is engineered through exponential growth in your yield-on-cost.

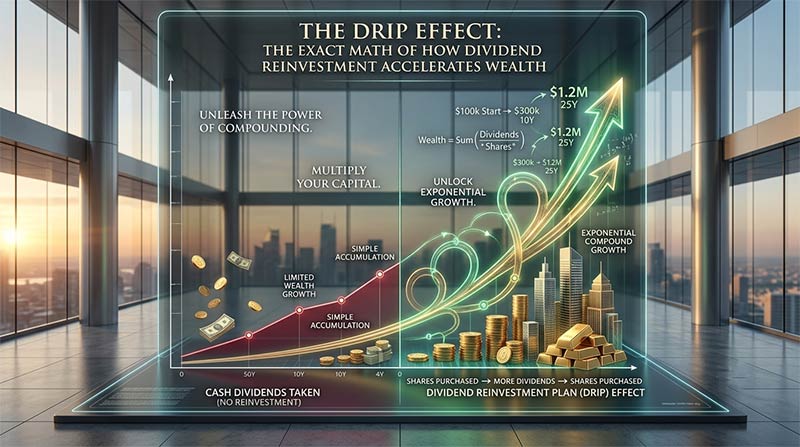

The Core Math: Yield vs. Dividend Growth

When an equity’s yield looks too good to be true, it almost always is. In mid-2026, several troubled Business Development Companies (BDCs) and structurally challenged REITs boast paper yields north of 15%. This is almost exclusively a function of a shrinking denominator—collapsing stock prices pumping up historical yield figures right before an inevitable dividend cut.

Sustainable wealth accumulation relies instead on compounding dividend growth. When a high-quality firm consistently grows its payout by 7% to 12% annually, your personal yield relative to your initial investment scales aggressively over a multi-year horizon.

As shown in the structural timeline above, the divergence between linear returns and a true compounding trajectory accelerates dramatically after the first few years. Reinvesting growing dividends back into discounted shares creates a self-funding flywheel that functions independently of temporary market corrections.

High-Conviction Dividend Growers for 2026

To survive the valuation pressures of the current market, a company must possess an ironclad economic moat and a payout strictly secured by free cash flow (FCF). According to mid-2026 research from asset management leaders like Morningstar and Fidelity, three distinct corporate profiles offer an optimal mix of safety, discount to fair value, and consistent distribution growth.

1. The Moat Defender: Clorox (CLX)

- The Thesis: After a prolonged period of operational restructuring, Clorox has emerged as one of the most deeply discounted consumer defensive assets on the board. Trading at a massive discount to its long-term intrinsic value estimate, its portfolio of dominant household brands provides highly inelastic pricing power.

- Dividend Health: Management’s long-term target remains a 60% payout ratio, leaving plenty of retained earnings to defend its market share while sustaining mid-single-digit annualized dividend hikes.

2. The Cliff Survivor: AbbVie (ABBV)

- The Thesis: For years, the market discounted AbbVie due to fears surrounding the Humira patent expiration. By mid-2026, those fears have been thoroughly answered. Growth from next-generation therapeutics has officially neutralized the legacy revenue drag, proving the durability of their underlying R&D engine.

- Dividend Health: Boasting over 50 consecutive years of dividend growth (dating back to its time as part of Abbott Laboratories), its forward yield sits well above the S&P 500 average, supported by a rapid return to positive organic earnings growth.

3. The Industrial Compounder: Watsco (WSO)

- The Thesis: As the largest HVAC and refrigeration distributor in North America, Watsco operates a highly fragmented distribution network that functions as a structural monopoly in key geographic corridors.

- Dividend Health: Watsco recently cleared the air with a strong 10% dividend hike. Uniquely, the company intentionally shuns share buybacks, choosing instead to reward its high insider ownership directly via cash distributions. While its trailing payout can look elevated relative to pure GAAP earnings, its actual cash-flow coverage remains pristine.

2026 Dividend Allocation Matrix

The table below contrasts these structural growth plays against the broader market parameters to help identify where capital should be allocated depending on your explicit risk tolerance.

| Stock Ticker | Primary Sector | Economic Moat Rating | Forward Dividend Yield | 5-Year Dividend Growth Rate (Avg) |

| Clorox (CLX) | Consumer Defensive | Wide | ~5.5% | Mid-Single Digit |

| Medtronic (MDT) | Healthcare | Narrow | ~3.8% | Low-to-Mid Single Digit |

| AbbVie (ABBV) | Healthcare / Biotech | Wide | ~3.3% | High-Single Digit |

| Watsco (WSO) | Industrials | Narrow | ~3.1% | ~11.1% |

| Sysco (SYY) | Food Distribution | Wide | ~3.0% | ~3.5% |

The Risk Filter: The Only Metrics That Matter Now

If you are auditing your portfolio for the back half of 2026, ignore historical accounting metrics and look solely at forward-looking liquidity filters:

- Free Cash Flow Payout Ratio less than 70%: Traditional net income payout ratios are easily distorted by non-cash charges and amortization. If a company’s dividend consumes more than 70% of its actual free cash flow, its ability to fund internal R&D or debt servicing during a macro downturn is compromised.

- Oligopolistic Pricing Power: In a stickier inflationary cycle, you want companies that distribute essential goods. If a firm cannot raise prices without losing 15% of its volume, its dividend growth is effectively dead on arrival. Look for industries dominated by three or fewer major players.

True passive wealth isn’t a lottery ticket; it is a calculated cash-flow model. Focus on the compounders trading at a discount today, automate the reinvestment process, and let the broader market wrestle with speculative valuations while your baseline income scales automatically.

Want to Make Money From Home ?

Join 55,000+ real, remote ways to make money every week.

Good luck! I hope you find the perfect remote opportunity for your lifestyle and goals.