The old rule of wealth building was frustratingly simple: you need money to make money. For decades, dividend investing was a playground reserved for people who already had substantial capital. If a solid blue-chip stock cost $350 a share and you only had $50 to invest at the end of the month, you were priced out of the game.

That structural barrier no longer exists. Today, the combination of zero-commission trading, micro-investing apps, and fractional shares has completely democratized cash-flow investing. You can build a highly diversified, yield-generating portfolio with the loose change left over from your grocery budget.

Here is exactly how to build a functional dividend machine on a shoestring budget without falling into high-yield traps.

The Two Mechanics That Leveled the Playing Field

To invest effectively with small amounts of money, you rely on two execution mechanisms that didn’t exist a generation ago:

- Fractional Shares: Instead of saving up for months to buy a single share of a premium stock or Exchange-Traded Fund (ETF), brokerages now let you buy slices of a share based on dollar amount rather than share volume. If you have $10, you can buy $10 worth of a company, even if its single share price is $300. You still receive your exact pro-rata share of the dividend. Platforms like Charles Schwab’s fractional trading framework allow you to split small deposits across multiple assets instantly.

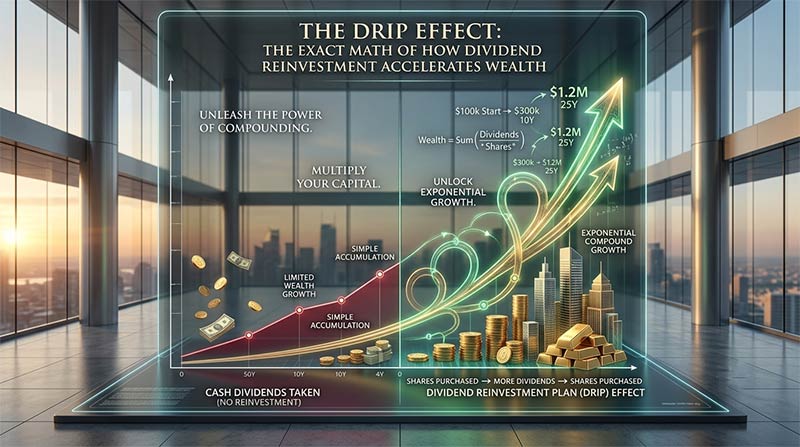

- Automated Dividend Reinvestment Plans (DRIP): When you own a tiny slice of a company, your quarterly dividend payout might only be $0.45. If that cash sits idle in your account, it does nothing. Enabling DRIP instructs your brokerage to automatically take that cash the moment it lands and buy more fractional slices of the asset that paid it. This triggers a continuous compounding loop without manual intervention or extra transaction fees.

Why Individual Stocks Are a Trap for Small Budgets

When starting with a small budget, the temptation is to hunt for individual high-yield stocks—companies promising 8%, 10%, or even 12% annual distributions. This is almost always a mistake known as a yield trap.

An unsustainably high dividend yield is frequently a sign of a company in deep financial distress, where the stock price has plummeted while the historical dividend hasn’t been cut yet. When the cut inevitably happens, you lose both your income stream and your underlying capital.

Furthermore, true diversification requires holding at least 20 to 30 companies across distinct market sectors (utilities, consumer staples, healthcare, tech). Managing that manually with $50 a month is an administrative headache.

The cleaner, safer solution is to use low-cost, dividend-focused ETFs. A single purchase instantly distributes your $10 or $20 across hundreds of vetted, cash-generating corporations.

Core Dividend Toolkits

When evaluating funds, look for a low expense ratio (the annual fee the fund charges to manage your money) and a solid track record of distribution growth.

| ETF Name | Ticker | Expense Ratio | Distribution Strategy |

| Schwab U.S. Dividend Equity ETF | SCHD | 0.06% | Focuses on fundamental financial health, cash flow, and steady dividend growth history. |

| Vanguard High Dividend Yield ETF | VYM | 0.04% | Tracks higher-yielding U.S. companies while maintaining extreme low-cost efficiency. |

| iShares Select Dividend ETF | DVY | 0.38% | Focuses on a tighter basket of roughly 100 U.S. stocks with a 5-year track record of consistent payouts. |

Note: For a deeper dive into fund metrics and current distributions, look through Morningstar’s high-yield analysis or review the specific asset breakdowns via Vanguard’s VYM fund guide.

The Execution Framework: Step-by-Step

Building this out requires a mechanical approach. Emotions and market timing matter far less than consistency.

- Automate Your Deposit: Treat your portfolio like a mandatory bill. Set up a recurring transfer of $10, $25, or $50 every single week or payday. The key is to remove the choice of whether or not to invest.

- Deploy Dollar-Cost Averaging: Do not wait for a market dip. Buy your chosen dividend ETF on the same day every month, regardless of whether the market is up or down. When prices are high, your fixed dollar amount buys fewer shares; when prices drop, your dollar amount automatically buys more shares.

- Turn On DRIP: Ensure your brokerage account settings have automated dividend reinvestment activated for every asset you buy.

The Reality of Scale

Let’s look at the math clearly, stripped of any get-rich-quick illusions. If you invest $50 a month into a diversified dividend fund yielding 3.5%, your first year will net you less than $25 in total dividend income.

That sounds insignificant. But the goal of small-budget dividend investing isn’t immediate wealth—it is building an automated system. Over time, as your monthly deposits continue and your dividends automatically buy more shares that pay more dividends, the growth curve shifts from linear to exponential. Your system scales up, converting pocket change into a meaningful, resilient income stream.

Want to Make Money From Home ?

Join 55,000+ real, remote ways to make money every week.

Good luck! I hope you find the perfect remote opportunity for your lifestyle and goals.